A Broker Price Opinion is an Opinion of Value for a property, " done by a local real estate professional or any other qualified company or real estate agent. BPOs are less expensive and are used to give an indication of the fair market value of a property.When providing the price opinion, brokers will consider the value of similar surrounding properties, sales trends prevalent in the adjacent neighborhood and any costs incurred in preparing the property for sale during a short sale or foreclosure.

A Broker Price Opinion is an Opinion of Value for a property, " done by a local real estate professional or any other qualified company or real estate agent. BPOs are less expensive and are used to give an indication of the fair market value of a property.When providing the price opinion, brokers will consider the value of similar surrounding properties, sales trends prevalent in the adjacent neighborhood and any costs incurred in preparing the property for sale during a short sale or foreclosure.

The Difference Between Appraisals and BPOs

Although BPOs serve the same purpose as appraisals, the main difference is that appraisals are done by licensed appraisers and lead to a deeper analysis of the property. They are hence costly and more time consuming. Banks prefer BPOs for their lower cost and faster results.

Some of the things contained in a BPO are:

Exterior and Interior conditions of the property – Most BPOs evaluate the exterior conditions of the property and then file a report. A thorough BPO report should also contain interior evaluations with specific attention to detail needed to capture any defects. Photos and historical data must also be collected to advise the final estimate.

Comparing with similar Properties – A BPO report should include comparison data for at least three similar properties currently on ale in the same market and three other properties that have been recently sold typically in the last 3 months.These properties should be located within a 1 mile radius of the subject property.

Above Ground Living Area (AGLA) should be approximately +/-10% of the property under evaluation. This is mainly because finished basements are evaluated with lower weighting factor compared to property with an above ground living area.

Neighborhood Data – the BPO report should include the neighborhood statistics, useful to banks in giving a better understanding of what the market situation is currently.These conditions can point into a declining market or a stable one.

Repairs Sheet- the real estate agent should provide an estimate of what it would cost to repair any damages to the house.

Value Estimate – By basing values on recent sales of comparable property, the real estate agent will provide a 'quick sale' estimates of what the property can fetch in 90-120 days in the market.

In case you need a broker price opinion agent in the Seattle/Eastside area, contact Hamid. Clients who contact him before end of the month qualify for free CMA.

Buying a new home is a huge commitment that requires careful planning and a good understanding of what the market is offering. It is usually advisable to hire the services of a real estate agent. Either way, here are some tips that you can use to navigate the complex yet very rewarding real estate market.

Buying a new home is a huge commitment that requires careful planning and a good understanding of what the market is offering. It is usually advisable to hire the services of a real estate agent. Either way, here are some tips that you can use to navigate the complex yet very rewarding real estate market. Given the nature of a condominium, mortgage lenders may have a stricter guideline when advancing credit to you. A condominium is an apartment that the owner owns as opposed to renting. Commonly, a condominium owner still shares the amenities in the apartment building with other owners but is legally entitled to their apartment.

Given the nature of a condominium, mortgage lenders may have a stricter guideline when advancing credit to you. A condominium is an apartment that the owner owns as opposed to renting. Commonly, a condominium owner still shares the amenities in the apartment building with other owners but is legally entitled to their apartment. Congratulations for moving into your new home. Moving can be a tiring period of frantic work and readjustment. As you settle down, we have compiled a checklist that you can use to ensure you get up to speed in your new home with ease.

Congratulations for moving into your new home. Moving can be a tiring period of frantic work and readjustment. As you settle down, we have compiled a checklist that you can use to ensure you get up to speed in your new home with ease. If you have been looking to buy a home recently, chances are you have heard the words "Short Sale" floating around quite a bit. In fact, in some markets, as many as 75% or so of homes on the market are advertised as "short sales". The truth is, that short sales, approved short sales, and the like are a bit of a complicated process, but hopefully today we can clear up some of that confusion for you.

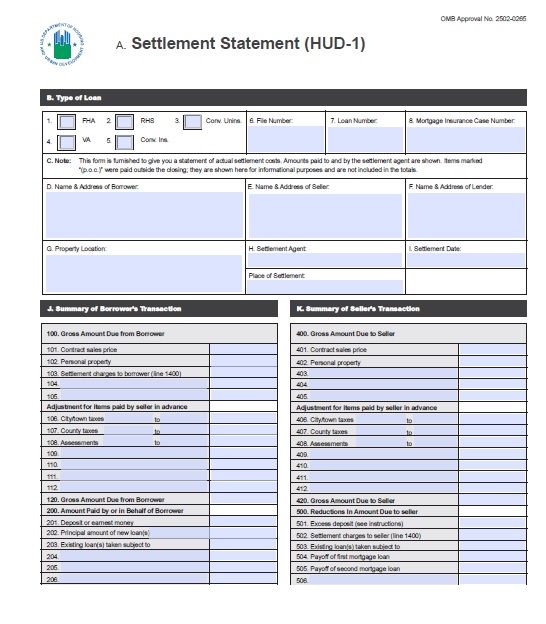

If you have been looking to buy a home recently, chances are you have heard the words "Short Sale" floating around quite a bit. In fact, in some markets, as many as 75% or so of homes on the market are advertised as "short sales". The truth is, that short sales, approved short sales, and the like are a bit of a complicated process, but hopefully today we can clear up some of that confusion for you. If you are buying a home, you should get used to hearing the term Hud-1 Settlement Statement. You will be hearing a lot about it on your home buying journey and it can be a little bit confusing, to say the least. Today we are going to try to navigate through the Hud-1 Settlement Statement to try to help you understand a bit more about it.

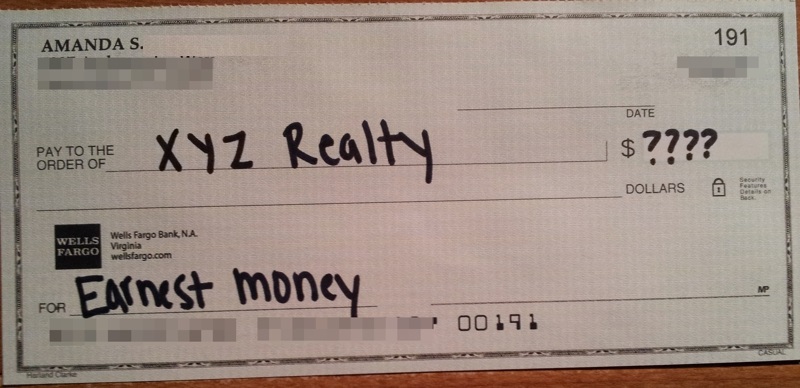

If you are buying a home, you should get used to hearing the term Hud-1 Settlement Statement. You will be hearing a lot about it on your home buying journey and it can be a little bit confusing, to say the least. Today we are going to try to navigate through the Hud-1 Settlement Statement to try to help you understand a bit more about it. Earnest Money. You may have heard the term before, but perhaps you aren't sure what it actually means. Sometimes it is referred to as simply earnest, or as an earnest payment. Today we are going to tell you everything you need to know about earnest money. Earnest money is essentially a deposit made by a potential home buyer to show interest in the property and to impress the seller. It is meant to show good faith in a real estate transaction and to show the seller that the potential buyer is "earnestly" interested in purchasing the property. Earnest money is not a down payment, and should not be confused as such. It is money paid in addition to a down payment, or a fraction of your down payment is a good way to look at it.

Earnest Money. You may have heard the term before, but perhaps you aren't sure what it actually means. Sometimes it is referred to as simply earnest, or as an earnest payment. Today we are going to tell you everything you need to know about earnest money. Earnest money is essentially a deposit made by a potential home buyer to show interest in the property and to impress the seller. It is meant to show good faith in a real estate transaction and to show the seller that the potential buyer is "earnestly" interested in purchasing the property. Earnest money is not a down payment, and should not be confused as such. It is money paid in addition to a down payment, or a fraction of your down payment is a good way to look at it.