There are many terms associated with the buying and selling of homes which very few home buyers are fully aware of but should be. One of those terms is a “mortgage rate lock”. To give you a better idea of what exactly they encompass, here's everything you need to know about mortgage rate locks as a home buyer.

What Is A Mortgage Rate Lock?

A mortgage rate lock is simply defined as the lender's promise to lock in a certain interest rate for a particular amount of time. This is usually done in order to ensure buyers can lock the interest rate quoted to them by the lender while going through the lengthy application process. There are a few different options when it comes to locking in your mortgage rate. A contract for a locked rate with locked points means that both the interest rate and the number of points paid upfront cannot change. A contract with a locked rate and floating points means that the lender must offer you the same interest rate initially determined, but they have the ability to charge you a different number of points at closing. If you get a mortgage rate lock that has a floating rate and floating points, this means you have the opportunity to lock in your rate and points in the time between the application submission and the final settlement.

Why Should I Get A Mortgage Rate Lock?

The number one reason why you should get a mortgage rate lock when purchasing a property is because the real estate market and mortgage rates change day to day, if not hour to hour. You don't necessarily know how long the application process will take, so it's best to lock in your rate and points in order to get the very best deal. You may have to pay more upfront, but you'll be saving yourself a whole lot more money in the long run.

How Much Does A Mortgage Rate Lock Cost?

The cost of a mortgage rate lock can vary as lenders are able to set their own rules. Some lenders will charge you an upfront fee to lock in the rates but won't return the fee if the application is denied or if you close the loan. On the other hand, some lenders will charge you the locking fee only once the loan is closed. They may also charge an extra fee to lock a rate for an extended period of time.

What's Included In A Mortgage Rate Lock Contract?

If you decide to purchase a mortgage rate lock, it's important to make sure that the contract between you and the lender clearly lays out the details of the agreement. It should include the precise terms of the lock, the lock's effective date, the expiration date and time of the lock, the costs and fees associated with the lock and any post-lock options.

Buying a home and dealing with mortgage rates that are constantly changing can be quite daunting, but it doesn't have to be. Now that you know everything you need to know about mortgage rate locks, you can feel confident discussing and negotiating rate terms with your lender.

A Broker Price Opinion is an Opinion of Value for a property, " done by a local real estate professional or any other qualified company or real estate agent. BPOs are less expensive and are used to give an indication of the fair market value of a property.When providing the price opinion, brokers will consider the value of similar surrounding properties, sales trends prevalent in the adjacent neighborhood and any costs incurred in preparing the property for sale during a short sale or foreclosure.

A Broker Price Opinion is an Opinion of Value for a property, " done by a local real estate professional or any other qualified company or real estate agent. BPOs are less expensive and are used to give an indication of the fair market value of a property.When providing the price opinion, brokers will consider the value of similar surrounding properties, sales trends prevalent in the adjacent neighborhood and any costs incurred in preparing the property for sale during a short sale or foreclosure. Buying a new home is a huge commitment that requires careful planning and a good understanding of what the market is offering. It is usually advisable to hire the services of a real estate agent. Either way, here are some tips that you can use to navigate the complex yet very rewarding real estate market.

Buying a new home is a huge commitment that requires careful planning and a good understanding of what the market is offering. It is usually advisable to hire the services of a real estate agent. Either way, here are some tips that you can use to navigate the complex yet very rewarding real estate market. Given the nature of a condominium, mortgage lenders may have a stricter guideline when advancing credit to you. A condominium is an apartment that the owner owns as opposed to renting. Commonly, a condominium owner still shares the amenities in the apartment building with other owners but is legally entitled to their apartment.

Given the nature of a condominium, mortgage lenders may have a stricter guideline when advancing credit to you. A condominium is an apartment that the owner owns as opposed to renting. Commonly, a condominium owner still shares the amenities in the apartment building with other owners but is legally entitled to their apartment. Congratulations for moving into your new home. Moving can be a tiring period of frantic work and readjustment. As you settle down, we have compiled a checklist that you can use to ensure you get up to speed in your new home with ease.

Congratulations for moving into your new home. Moving can be a tiring period of frantic work and readjustment. As you settle down, we have compiled a checklist that you can use to ensure you get up to speed in your new home with ease. If you have been looking to buy a home recently, chances are you have heard the words "Short Sale" floating around quite a bit. In fact, in some markets, as many as 75% or so of homes on the market are advertised as "short sales". The truth is, that short sales, approved short sales, and the like are a bit of a complicated process, but hopefully today we can clear up some of that confusion for you.

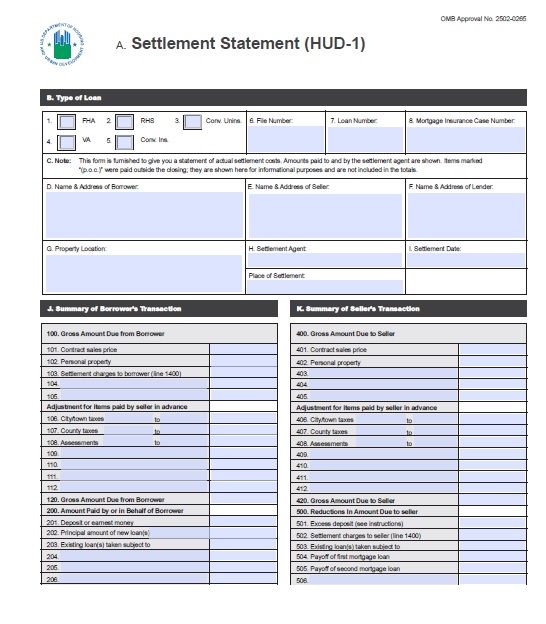

If you have been looking to buy a home recently, chances are you have heard the words "Short Sale" floating around quite a bit. In fact, in some markets, as many as 75% or so of homes on the market are advertised as "short sales". The truth is, that short sales, approved short sales, and the like are a bit of a complicated process, but hopefully today we can clear up some of that confusion for you. If you are buying a home, you should get used to hearing the term Hud-1 Settlement Statement. You will be hearing a lot about it on your home buying journey and it can be a little bit confusing, to say the least. Today we are going to try to navigate through the Hud-1 Settlement Statement to try to help you understand a bit more about it.

If you are buying a home, you should get used to hearing the term Hud-1 Settlement Statement. You will be hearing a lot about it on your home buying journey and it can be a little bit confusing, to say the least. Today we are going to try to navigate through the Hud-1 Settlement Statement to try to help you understand a bit more about it.