So, it is time! You have found the home of your dreams, and you are sure it is the perfect one! You have your earnest money ready, you are pre-qualified for your loan, and now it is time for that all important step: making an offer! This article will give you more details about the process of making an offer on a home, and will help you with any questions that you might have.

The first step is meeting with your agent. You and your agent will come up with a reasonable offer based on factors such as the selling prices of similar homes in the area, how long the home has been on the market, etc. You will then need to fill out a Purchase Agreement Form. You need to be prepared with a lot of information, because the Purchase Agreement Form requires a lot of detailed information about the property that you are wanting to purchase. Your real estate agent will be help you with this information and assist you in filling out the forms.

There are a few different things that will have to be included in your offer. Here is a short list:

Pre-Approval Letter From Mortgage Company

You will need to pre-approved for your loan prior to writing the offer (or have proof of funds if you are not going to be needing financing). You will need to have the pre-approval letter from your mortgage lender to give to your agent. They will in turn pass it onto the seller's agent. You will have to include this along with the mode of financing, and the percentage you want to put down. Also include whether or not you want the seller to pay any closing costs.

Earnest Money

You will need to have your earnest money ready to make a good impression and show the seller that you are serious about buying the property. It is usually 3-5% of the purchase price, but your agent can help you decide on just the right amount.

Price

You will also have to include the price that you are offering to pay for the property. Remember that the price listed is not what you have to offer, but only indicates what the seller is willing to accept at the current point and time. It is not a bad idea to offer less than the listing price if you can not afford the listing price. There is always the chance that the seller can say no, but there is also the chance that they can say yes!

Possession.

You must include when you wish to take possession of the property. Usually this is done immediately after closing, but might be a different day if there are unusual circumstances. You also need to include any personal possessions that you want the seller to include, such as window treatments, appliances, etc..

Closing Date

You also will need to specify which date you would like to transfer ownership of the property, or close on the property. This is usually within 3-10 weeks. This is where you will sign the final papers on your property, have certified funds, and take ownership. You also need to include whether or not you will have an inspection done. This is usually done within 3-5 days of an agreement being reached.

Contingency, Miscellaneous

If you are going to have any contingencies for the purchase of the property, such as a title contingency or a sale that is contingent on the sale of another property, you will need to list that in the offer. Also you will need to include any miscellaneous items, such as a home warranty or obligation for city inspection if one is required. You will also need to include a seller disclosure form, where the seller answers specific questions about the property. You will also need the legal description of the property, which is the written words describing a properties exact location. This is much different than the street address.

After your offer is submitted, it becomes a waiting game. Usually you will know something within 24 hours. The seller can either accept your offer, and you will then move forward in the home buying process, or reject your offer. The seller also has the option to counter your offer with a proposed amendment. It is important to remember not to engage in a "bidding war" with other potential buyers and end up bidding more than you can afford. You have to know when to walk away.

If you are looking for a real estate agent that can help you write up an offer, or if you just have questions about the offer process or the home buying process in general, we can help you! Contact Hamid Ali today for all of your real estate needs!

One of the most common types of contingency that you will see in a purchase and sale agreement is an inspection contingency. Buying a home could be the largest single investment you will ever make. To minimize unpleasant surprises and unexpected difficulties, you’ll want to learn as much as you can about the newly constructed or existing house before you buy it. If you are buying a home in Washington state, home purchases are contingent upon inspection.

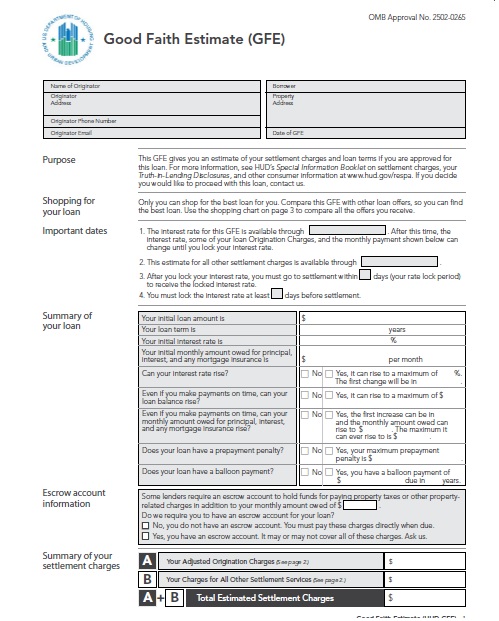

One of the most common types of contingency that you will see in a purchase and sale agreement is an inspection contingency. Buying a home could be the largest single investment you will ever make. To minimize unpleasant surprises and unexpected difficulties, you’ll want to learn as much as you can about the newly constructed or existing house before you buy it. If you are buying a home in Washington state, home purchases are contingent upon inspection. A good faith estimate is often referred to as a GFE. The GFE is provided by the mortgage lender or broker to the customer and is required by the Real Estate Settlement Procedures Act, also known as RESPA. It is an estimate of the loan fees or “closing costs” for the customer’s mortgage.

A good faith estimate is often referred to as a GFE. The GFE is provided by the mortgage lender or broker to the customer and is required by the Real Estate Settlement Procedures Act, also known as RESPA. It is an estimate of the loan fees or “closing costs” for the customer’s mortgage.