Given the nature of a condominium, mortgage lenders may have a stricter guideline when advancing credit to you. A condominium is an apartment that the owner owns as opposed to renting. Commonly, a condominium owner still shares the amenities in the apartment building with other owners but is legally entitled to their apartment.

Given the nature of a condominium, mortgage lenders may have a stricter guideline when advancing credit to you. A condominium is an apartment that the owner owns as opposed to renting. Commonly, a condominium owner still shares the amenities in the apartment building with other owners but is legally entitled to their apartment.

It is important to understand the regulations that lenders have before looking for a mortgage for the condo.This is important especially if you plan to resell the condo as potential buyers will want to understand the loan condition of the condo. In case you want some help on this you can contact a mortgage loan administrator for specific guidelines for particular mortgage products.

Ensure the Condo Federal Housing Administration Approved – Federal Housing Administration (FHA) loans are frequently being used right now by borrowers with less down payment money available.Ensuring that the condo is FHA loan approved allows you to use the loan service when buying or for any potential buyers to use the service when you resell.

Beware of Building Rental Limits – Simply put, can you move out and rent the condo to someone else? This is vital for two reasons, in case you already have a house and want to use the condo as an extra source of income then it should not have rental limits and two, in case you resell, you potential buyers may be turned off by rental limit clauses.However, the bank may not see it this way and would rather extend a loan to an owner’s only condo.

Check for Pending/Active Litigation – Condos that have open cases in court will not attract any mortgages. this is because the case can result in change of ownership of the complex. Because case can take years to complete, you are better off looking elsewhere in case you are in a hurry or don't mind something else.Also be careful in case the condo oeners are considering possible litigation.

Check for the Rate of Defaulters– Some mortgage institutions have tight regulations or the number of adjacent condo owners that can be ion default in the complex at any particular time to their Home Owners Association (HOA) dues. Reviewing HOA documentation is a good precaution against this.

Go Through the Reserve Study and HOA Future Repair Funds – Condos are annually checked for the lifespan of the various installed systems and the expected costs for repair matched against the HOA funds reserved for this purpose,. In case the reserves are low, mortgage lenders may not advance you a mortgage. You must also ensure that the HOA reserves for the condo you are planing to buy are adequate to avoid rejection by a mortgage lender.

In case you are in the market to buy or sell a condo in Eastside, WA, please contact Hamid for assistance and consultation on the email and telephone number provided.

Congratulations for moving into your new home. Moving can be a tiring period of frantic work and readjustment. As you settle down, we have compiled a checklist that you can use to ensure you get up to speed in your new home with ease.

Congratulations for moving into your new home. Moving can be a tiring period of frantic work and readjustment. As you settle down, we have compiled a checklist that you can use to ensure you get up to speed in your new home with ease. If you have been looking to buy a home recently, chances are you have heard the words "Short Sale" floating around quite a bit. In fact, in some markets, as many as 75% or so of homes on the market are advertised as "short sales". The truth is, that short sales, approved short sales, and the like are a bit of a complicated process, but hopefully today we can clear up some of that confusion for you.

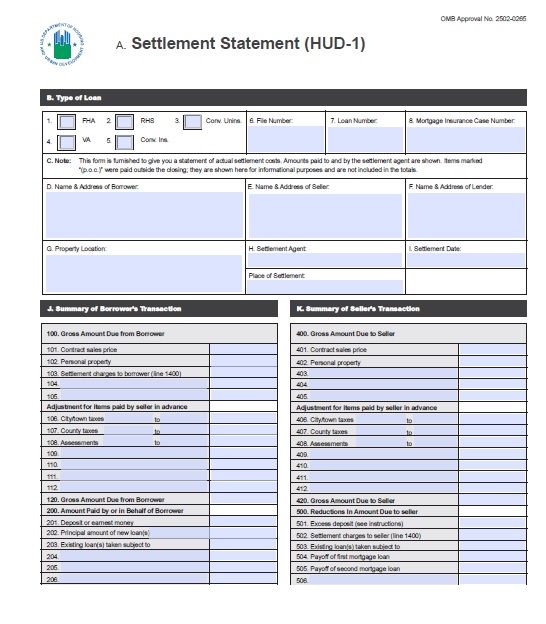

If you have been looking to buy a home recently, chances are you have heard the words "Short Sale" floating around quite a bit. In fact, in some markets, as many as 75% or so of homes on the market are advertised as "short sales". The truth is, that short sales, approved short sales, and the like are a bit of a complicated process, but hopefully today we can clear up some of that confusion for you. If you are buying a home, you should get used to hearing the term Hud-1 Settlement Statement. You will be hearing a lot about it on your home buying journey and it can be a little bit confusing, to say the least. Today we are going to try to navigate through the Hud-1 Settlement Statement to try to help you understand a bit more about it.

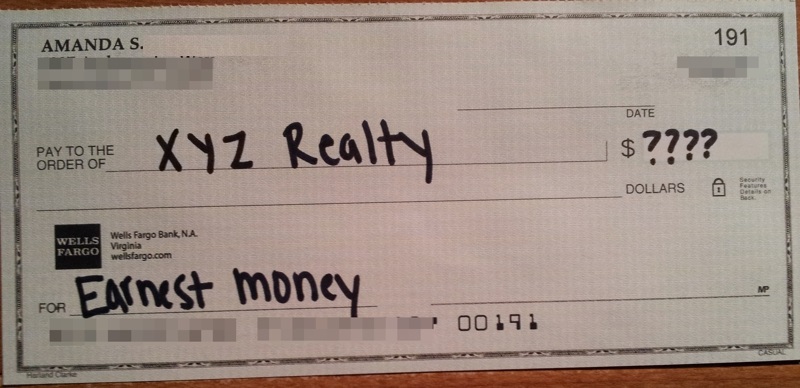

If you are buying a home, you should get used to hearing the term Hud-1 Settlement Statement. You will be hearing a lot about it on your home buying journey and it can be a little bit confusing, to say the least. Today we are going to try to navigate through the Hud-1 Settlement Statement to try to help you understand a bit more about it. Earnest Money. You may have heard the term before, but perhaps you aren't sure what it actually means. Sometimes it is referred to as simply earnest, or as an earnest payment. Today we are going to tell you everything you need to know about earnest money. Earnest money is essentially a deposit made by a potential home buyer to show interest in the property and to impress the seller. It is meant to show good faith in a real estate transaction and to show the seller that the potential buyer is "earnestly" interested in purchasing the property. Earnest money is not a down payment, and should not be confused as such. It is money paid in addition to a down payment, or a fraction of your down payment is a good way to look at it.

Earnest Money. You may have heard the term before, but perhaps you aren't sure what it actually means. Sometimes it is referred to as simply earnest, or as an earnest payment. Today we are going to tell you everything you need to know about earnest money. Earnest money is essentially a deposit made by a potential home buyer to show interest in the property and to impress the seller. It is meant to show good faith in a real estate transaction and to show the seller that the potential buyer is "earnestly" interested in purchasing the property. Earnest money is not a down payment, and should not be confused as such. It is money paid in addition to a down payment, or a fraction of your down payment is a good way to look at it. When you are buying a home, you might also have to join a homeowner's association. One thing you definitely need to do is evaluate your homeowner's association. You need to know what you are getting into, and what will be expected of you. When purchasing a home that is part of a homeowner's association, you will receive a packet of documents detailing the rules, etc. of the homeowner's association. This packet is usually called the "Public Offering Statement". Today we are going to share some tips with you on how to manage those documents and make your own evaluations of the health of a homeowner's association.

When you are buying a home, you might also have to join a homeowner's association. One thing you definitely need to do is evaluate your homeowner's association. You need to know what you are getting into, and what will be expected of you. When purchasing a home that is part of a homeowner's association, you will receive a packet of documents detailing the rules, etc. of the homeowner's association. This packet is usually called the "Public Offering Statement". Today we are going to share some tips with you on how to manage those documents and make your own evaluations of the health of a homeowner's association.