If you are buying a home, you should get used to hearing the term Hud-1 Settlement Statement. You will be hearing a lot about it on your home buying journey and it can be a little bit confusing, to say the least. Today we are going to try to navigate through the Hud-1 Settlement Statement to try to help you understand a bit more about it.

If you are buying a home, you should get used to hearing the term Hud-1 Settlement Statement. You will be hearing a lot about it on your home buying journey and it can be a little bit confusing, to say the least. Today we are going to try to navigate through the Hud-1 Settlement Statement to try to help you understand a bit more about it.

HUD is the government branch for Housing and Urban Development. The folks at HUD handle all housing, home ownership and development of property legislation in the USA. The HUD-1 Settlement Statement is a three page document that every home buyer receives when they borrow money to purchase a home or property. You may also hear the HUD-1 Settlement Statement referred to as simply the Hud-1,Settlement Statement, Closing Sheet, or Closing Statement. All of these terms refer to the same document.

When you get the HUD-1 Statement, you should take pride in knowing it is one of the final steps before becoming a certified homeowner. The HUD-1 will be used by the closing agent as a way to itemize and explain all fees associated with your home loan. The point of the HUD-1 is to give both the buyer and the seller a detailed list of all of their incoming and outgoing funds.

You must receive the HUD-1 at least one day before closing on your new home. You need to make very sure to review the documents carefully before closing, both on your own, and with your agent. You want to make sure that there are no errors, and that all the facts and figures on the Hud-1 match up to the figures you were provided with in your Good Faith Estimate. Make sure that you understand all of the figures completely before you sign off on it.

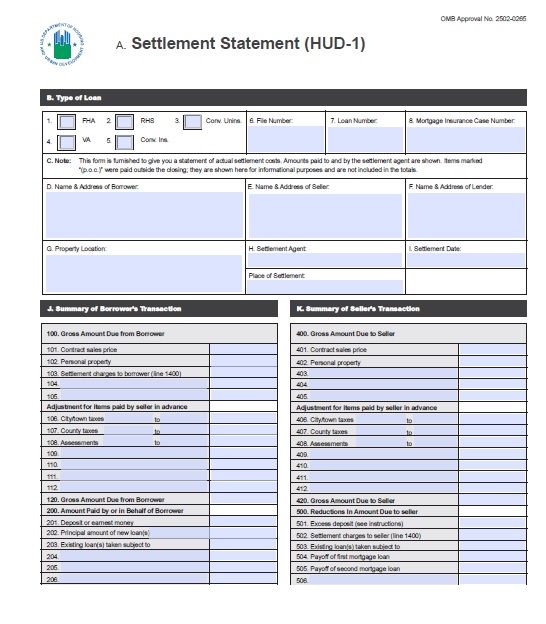

There are three pages to the Hud-1 Settlement Statement. The first page is a two column list. The buyer's details will be listed on the left hand side, and the seller's details on the right hand side. The first page is basically summarizing all of the fees and credits that are being processed during the transaction. Each line on the document is numbered, like something you might have seen before on income tax forms.

Some of the things you will find on the top of page one will be housekeeping information like the type of loan/loan ID number, all the personal contact information for the buyer and seller, etc. The next section will be numbered as the 100's which will detail the amounts due for the property, and a total that you owe for the purchase of the home. The next section is the 200's, which will detail the amount paid by the buyer or borrowed on behalf of the buyer, including any deposits and the principle amount of the loan. The 300's will detail the cash that is due from the buyer at closing. The 400's will detail the total amount due to the seller for the purchase of the home. The 500's will include any reductions such as closing costs, taxes, etc. The 600's will detail any cash at the settlement that is due to the seller or from the seller. That will conclude the first page of the HUD-1.

The second page of the HUD-1 is also a two column list, this time a detailed run down of all of the fees and charges associated with the closing of the property. The 700's will be all of your broker fees, the 800's are any items payable in connection with your loan, such as appraisal fee, credit report fee, etc.. The 900's are items that the lender requires to be paid in advance, such as interest charges, homeowner's insurance fees, etc. The 1000's are the reserves that are deposited with the lender. These include all of the escrow payments, etc. The 1100's will detail any title charges, while the 1200's will be for the transfer charges and government recording charges. The 1300's are reserved for additional settlement charges, and finally the 1400's will be the total settlement charges.

The third and final page of the HUD-1 is all about the Good Faith Estimate or GFE. The HUD charges will be listed right along side the GFE charges so it will be easy to spot anything that might be wrong, or any errors that you will need to take a look at. The very last section will detail all of the loan terms and a little more info about penalties. That will be the conclusion of your HUD-1 Settlement Statement. It may sound a bit confusing, but choosing a good real estate agent like Hamid Ali can help you navigate through the process much easier!

Speak Your Mind